Empower Your Audits with Statistical Sampling and Risk Analysis

In the intricate world of auditing, statistical sampling and risk analysis have become indispensable tools for enhancing audit efficiency and effectiveness. As auditors strive to navigate increasingly complex financial landscapes, the need for robust data analysis and risk assessment methods has never been greater. This exclusive article delves into the transformative power of statistical sampling and risk analysis in auditing, providing a comprehensive guide that will equip auditors with the knowledge and skills to excel in their field.

What is Statistical Sampling in Auditing?

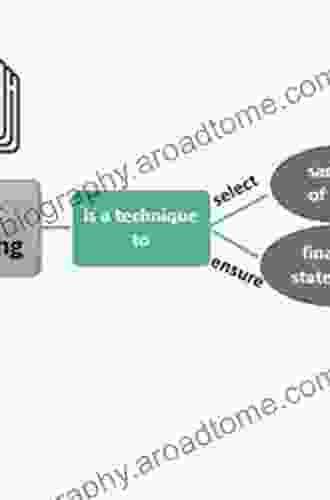

Statistical sampling involves the selection of a representative subset of data from a large population to draw inferences about the characteristics of the entire population. In auditing, statistical sampling enables auditors to examine a limited number of items within an account balance or transaction stream rather than scrutinizing each and every item. This streamlined approach allows auditors to obtain sufficient evidence to form an opinion about the accuracy and fairness of the financial statements while minimizing audit costs and time.

4 out of 5

| Language | : | English |

| File size | : | 2834 KB |

| Text-to-Speech | : | Enabled |

| Enhanced typesetting | : | Enabled |

| Word Wise | : | Enabled |

| Print length | : | 171 pages |

| Screen Reader | : | Supported |

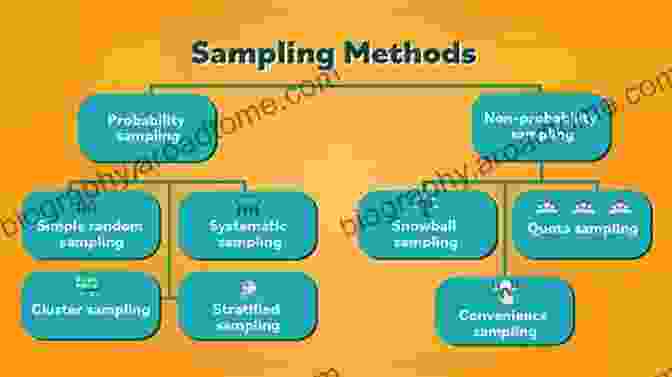

Types of Statistical Sampling Methods

There are various statistical sampling methods available for auditors, each with its own strengths and weaknesses. The choice of method depends on the specific audit objectives, data characteristics, and risk assessment. Some commonly used methods include:

- Random sampling: Each item in the population has an equal probability of being selected.

- Systematic sampling: Items are selected at regular intervals from the population.

- Stratified sampling: The population is divided into subgroups (strata),and then items are randomly selected from each stratum.

- Cluster sampling: Groups of items (clusters) are randomly selected, and then all items within the selected clusters are examined.

Benefits of Statistical Sampling in Auditing

The use of statistical sampling in auditing offers numerous advantages, including:

- Reduced audit costs: By examining a sample rather than the entire population, auditors can significantly reduce the time and resources required to perform an audit.

- Improved audit efficiency: Statistical sampling enables auditors to focus their efforts on areas of higher risk, leading to more efficient and targeted audit procedures.

- Enhanced audit quality: By using scientific sampling methods, auditors can increase the reliability and validity of their findings, resulting in higher quality audit reports.

- Objectivity and transparency: Statistical sampling provides an objective and transparent basis for drawing s about the population, minimizing the risk of bias or subjectivity.

Risk Analysis in Auditing

Risk analysis is an integral part of the audit process that helps auditors identify, assess, and mitigate potential risks that could impact the accuracy and completeness of the financial statements. By conducting a comprehensive risk assessment, auditors can prioritize their audit activities and allocate resources effectively.

Steps of Risk Analysis in Auditing

The risk analysis process typically involves the following steps:

- Risk identification: Auditors brainstorm and analyze potential risks that could affect the financial statements.

- Risk assessment: Auditors evaluate the likelihood and potential impact of each identified risk.

- Risk response: Auditors develop and implement strategies to mitigate or manage the identified risks.

- Risk monitoring: Auditors continuously monitor risks throughout the audit and make adjustments as needed.

Benefits of Risk Analysis in Auditing

Effective risk analysis in auditing provides numerous benefits, including:

- Improved audit planning: Risk analysis helps auditors prioritize their audit activities and allocate their resources more efficiently.

- Enhanced audit efficiency: By focusing on the most significant risks, auditors can streamline their audit procedures and minimize unnecessary testing.

- Reduced audit costs: Risk analysis enables auditors to identify and mitigate risks that could lead to costly audit delays or findings.

- Improved audit quality: By understanding and addressing risks, auditors can increase the likelihood of detecting material misstatements in the financial statements.

Statistical Sampling and Risk Analysis in Practice

To illustrate the practical application of statistical sampling and risk analysis in auditing, consider the following scenario:

An auditor is tasked with auditing the inventory account of a manufacturing company. The inventory account balance is significant, and the auditor is concerned about the potential for overstatement due to obsolete or slow-moving items. To address this risk, the auditor decides to use statistical sampling to select a sample of inventory items for physical inspection.

The auditor uses a stratified sampling method to select a sample of inventory items, ensuring that items from different product categories and locations are represented. The auditor then physically inspects the selected items and compares their condition and quantity to the inventory records. Based on the sample results, the auditor concludes that the inventory account balance is fairly stated.

This example demonstrates how statistical sampling and risk analysis can be combined to enhance the efficiency and effectiveness of an audit. By using a scientific sampling method and considering the potential risks, the auditor was able to obtain sufficient evidence to support their about the accuracy of the inventory account.

Statistical sampling and risk analysis are indispensable tools for modern auditors. By leveraging these techniques, auditors can significantly improve the efficiency, effectiveness, and quality of their audits. Through the use of statistical sampling, auditors can reduce costs and time while obtaining reliable evidence. Risk analysis enables auditors to prioritize their audit activities and focus on areas of higher risk, leading to more targeted and impactful audits.

As the auditing landscape continues to evolve, auditors must embrace statistical sampling and risk analysis as essential components of their toolkit. By mastering these techniques, auditors can enhance their professional capabilities and deliver exceptional audit services to their clients.

For further exploration of statistical sampling and risk analysis in auditing, consider reading the following comprehensive book:

Statistical Sampling And Risk Analysis In Auditing

This comprehensive guide provides a detailed overview of statistical sampling and risk analysis methods in auditing. It covers a wide range of topics, including:

- The theory and application of statistical sampling

- Different types of statistical sampling methods

- Risk assessment and risk response strategies

- Integrating statistical sampling and risk analysis into the audit process

- Case studies and examples of statistical sampling and risk analysis in practice

By investing in this book, auditors can gain a deep understanding of these essential auditing techniques and enhance their ability to deliver high-quality audits.

4 out of 5

| Language | : | English |

| File size | : | 2834 KB |

| Text-to-Speech | : | Enabled |

| Enhanced typesetting | : | Enabled |

| Word Wise | : | Enabled |

| Print length | : | 171 pages |

| Screen Reader | : | Supported |

Do you want to contribute by writing guest posts on this blog?

Please contact us and send us a resume of previous articles that you have written.

Book

Book Novel

Novel Page

Page Chapter

Chapter Text

Text Story

Story Genre

Genre Reader

Reader Library

Library Paperback

Paperback E-book

E-book Magazine

Magazine Newspaper

Newspaper Paragraph

Paragraph Sentence

Sentence Bookmark

Bookmark Shelf

Shelf Glossary

Glossary Bibliography

Bibliography Foreword

Foreword Preface

Preface Synopsis

Synopsis Annotation

Annotation Footnote

Footnote Manuscript

Manuscript Scroll

Scroll Codex

Codex Tome

Tome Bestseller

Bestseller Classics

Classics Library card

Library card Narrative

Narrative Biography

Biography Autobiography

Autobiography Memoir

Memoir Reference

Reference Encyclopedia

Encyclopedia Ronald T Kneusel

Ronald T Kneusel Charles R Swindoll

Charles R Swindoll Gary Morris

Gary Morris Logan Murray

Logan Murray Peter Baldwin Panagore

Peter Baldwin Panagore Michael Hearns

Michael Hearns Paul Lima

Paul Lima Jonathan Doherty

Jonathan Doherty Shifra Horn

Shifra Horn Terry Matlen

Terry Matlen J G Knox

J G Knox Elaine Heumann Gurian

Elaine Heumann Gurian Ingrid Loos Miller

Ingrid Loos Miller Sez Kristiansen

Sez Kristiansen Ella Dawson

Ella Dawson Augustus A White

Augustus A White Walter Kirn

Walter Kirn Daniel Defoe

Daniel Defoe Uta Frith

Uta Frith Matt Wiley

Matt Wiley

Light bulbAdvertise smarter! Our strategic ad space ensures maximum exposure. Reserve your spot today!

Terry PratchettPrinciples, Technologies, and Applications: The Essential Textile Handbook

Terry PratchettPrinciples, Technologies, and Applications: The Essential Textile Handbook Edgar HayesFollow ·10.1k

Edgar HayesFollow ·10.1k Nathaniel HawthorneFollow ·19.5k

Nathaniel HawthorneFollow ·19.5k Greg CoxFollow ·11k

Greg CoxFollow ·11k Israel BellFollow ·15.7k

Israel BellFollow ·15.7k Philip BellFollow ·19.8k

Philip BellFollow ·19.8k Robert ReedFollow ·10.8k

Robert ReedFollow ·10.8k Demetrius CarterFollow ·2.3k

Demetrius CarterFollow ·2.3k Garrett PowellFollow ·10.6k

Garrett PowellFollow ·10.6k

Ashton Reed

Ashton ReedUnveiling the Silent Pandemic: Bacterial Infections and...

Bacterial infections represent...

Brent Foster

Brent FosterFinally, Outcome Measurement Strategies Anyone Can...

In today's...

Brett Simmons

Brett SimmonsUnlocking the Secrets to Entrepreneurial Excellence:...

Empowering...

Joel Mitchell

Joel Mitchell

Kenzaburō Ōe

Kenzaburō Ōe

Eugene Powell

Eugene PowellOur Search For Uncle Kev: An Unforgettable Journey...

Prepare to be captivated by...

4 out of 5

| Language | : | English |

| File size | : | 2834 KB |

| Text-to-Speech | : | Enabled |

| Enhanced typesetting | : | Enabled |

| Word Wise | : | Enabled |

| Print length | : | 171 pages |

| Screen Reader | : | Supported |